The great strategic contests of the twenty-first century are not decided on battlefields alone. They are fought in container terminals and railway concessions, in the bandwidth of subsea cables, and in the carefully calibrated vocabulary of G20 Leaders’ Declarations. But they are also decided – often violently – by the wars that break out along the corridors themselves. The ongoing Iran-Israel-US military confrontation is not a parenthesis in the story of global infrastructure competition. It is one of its most consequential chapters.

Washington’s answer to China’s Belt and Road Initiative (BRI) is not a single project but a system of three interlocking corridor alliances: the India-Middle East-Europe Economic Corridor (IMEC) in the Gulf-Mediterranean arc, the Luzon Economic Corridor (LEC) in the Indo-Pacific, and the Zangezur Corridor in the South Caucasus. Each enrolls a distinct set of local partners. Each targets a distinct node of Chinese structural hegemony. And each is now being stress-tested – in different ways and with different results – by the strategic earthquake by the Iran war.

Weaponized Connectivity and the Three-Theatre Strategy

The intellectual framework underpinning Washington’s tripartite corridor strategy is what scholars call “weaponized interdependence”: the capacity of states positioned at the critical hub nodes of global networks to choke off access, gather intelligence, and coerce rivals by making economic connection itself a source of strategic leverage. China’s BRI is the most ambitious modern expression of this logic – a deliberate attempt to position Beijing at the junctions of global trade and energy flows across Eurasia, Africa, and the Indo-Pacific, acquiring both the ability to coerce specific targeted actors and the macro-level capacity to reshape third-party behavior through supply chain amplification.

Washington’s three corridors target distinct dimensions of that dominance. IMEC contests Chinese structural positioning in the Gulf-to-Mediterranean arc and the regional digital infrastructure where Huawei has penetrated deepest. The LEC displaces Chinese state capital from a strategically critical Indo-Pacific zone and integrates civilian logistics with allied naval capabilities. The Zangezur Corridor drives a Western-facilitated wedge into the Russia-Iran-China complementary logistics triangle in Central Asia, denying Moscow its historical role as the Caucasus’s security arbiter. Together they constitute a coherent spatial strategy – not three isolated projects but three flanks of a single connectivity war. What has changed since October 2023 is that one of those flanks is now also a shooting war.

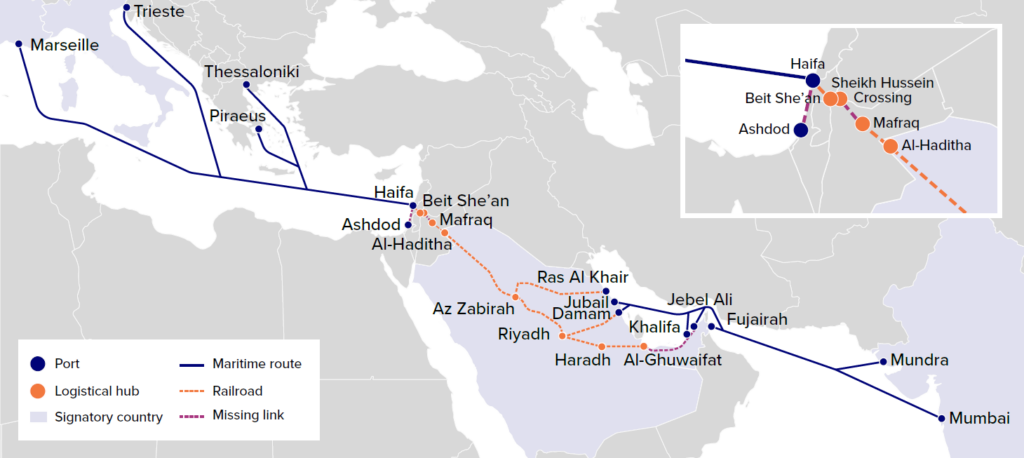

IMEC – The Corridor the War Is Trying to Break

IMEC was conceived as the most comprehensive US-aligned counter-architecture yet assembled against BRI: a multilateral coalition of nine actors – India, the United States, the EU, Saudi Arabia, the UAE, Jordan, Israel and Greece – connecting India to Europe via the Arabian Gulf, Israel, and the Eastern Mediterranean. Its design extended well beyond physical infrastructure: clean hydrogen pipelines, subsea electricity cables, and the Secure and Aligned AI Initiative (SAAII) to counter Chinese penetration of Gulf digital infrastructure. It was an explicit attempt to build new hub nodes – Jebel Ali, Aqaba, Haifa, Piraeus – that reduce the structural indispensability of Chinese-controlled logistics across the Eurasian trade system.

The Iran-Israel-US war has struck at IMEC’s most vulnerable seam. The corridor’s Northern arc – running from Saudi Arabia through Jordan and Israel to Greece – was premised on three political conditions: advancing Saudi-Israeli normalization, functioning Red Sea shipping lanes, and a stable Eastern Mediterranean security environment. The Hamas attacks of October 7, 2023, and the subsequent expansion of the conflict to encompass direct Iranian missile and drone strikes on Israeli territory – and on Gulf civilian infrastructure – have suspended all three simultaneously. Haifa’s Liner Shipping Connectivity Index fell 34.5% from its Q3 2023 peak. Red Sea Houthi attacks, directly enabled by Iranian logistics and intelligence, rerouted global shipping away from the Suez Canal and toward the Cape of Good Hope – paradoxically reinforcing the structural significance of Chinese-influenced Indian Ocean transshipment hubs that IMEC was designed to marginalize.

Yet the deeper story is more complex than a simple narrative of disruption. For the Gulf states – Saudi Arabia and the UAE above all – the Iranian strikes have shattered the foundational premise of a decade-long hedging strategy. For years, Riyadh and some Gulf states maintained a deliberate division of reliance: security and military affairs almost exclusively in the American orbit (a roughly 9:1 US advantage over China in advanced arms transfers to the region), while economic and infrastructural ties were increasingly oriented toward Beijing. The Chinese-brokered Saudi-Iranian normalization of 2023 was the clearest expression of this approach: a calculated wager that diplomatic engagement could purchase immunity from Iranian aggression. The missile barrages have demolished that wager. With containment-through-appeasement discredited, the Gulf states are being pushed toward active participation in a layered regional deterrence architecture alongside the United States and Israel – making IMEC’s political significance far larger than its commercial rationale alone. The corridor is no longer just a trade project. It is a statement of which side the Gulf is on.

Jordan and Greece illustrate the asymmetric costs of corridor membership. Jordan, the Northern Corridor’s indispensable transit state, suspended the UAE-Israel-Jordan Water-for-Energy deal in November 2023 under domestic political pressure – demonstrating how a small state on the edge of an active conflict theater can become an involuntary chokepoint. Greece faces a structural contradiction: Piraeus, IMEC’s western terminus, is majority-owned by COSCO, the Chinese state shipping company, making it simultaneously the corridor’s endpoint and BRI’s most important European node. The EU cannot credibly promote IMEC as a Western infrastructure alternative while its designated Mediterranean gateway remains Beijing-aligned. For India – the corridor’s most structurally committed partner, seeking emancipation from the Pakistan-CPEC chokehold on its westward trade access – IMEC’s disruption is a setback, not a reversal. India’s stake in the corridor is long-term and structural; no single conflict episode changes New Delhi’s fundamental interest in diversifying away from Chinese-influenced logistics.

Luzon – The Indo-Pacific Corridor the War Is Clarifying

The Luzon Economic Corridor, announced in April 2024 as a US-Japan-Philippines trilateral partnership under the G7’s Partnership for Global Infrastructure and Investment, tells a structurally different story. Here, the Iran-Israel-US war functions not as a disruption but as a clarifying force – sharpening the strategic logic that already drove Manila toward Washington.

The LEC’s origins lie in a political recapture: under President Duterte, the Subic-Clark Corridor was progressively integrated into China’s geoeconomic orbit through the $935 million Subic-Clark Railway, awarded to Chinese state-owned CCCC. That project collapsed under the weight of public distrust rooted in Chinese maritime aggression in the South China Sea. The Marcos Jr. administration cancelled it in 2023 and opened the space to US and Japanese capital – investments in rail, ports, agribusiness, and semiconductor supply chains that simultaneously serve civilian logistics and allied naval capabilities under the Enhanced Defense Cooperation Agreement. China has characterized the LEC as a “mini-NATO” in Southeast Asia – confirming that the corridor functions as spatial containment as much as economic development.

For the Philippines, the war in the Middle East has reinforced, rather than complicated, this pivot. As Iranian-backed Houthi attacks disrupted global shipping and exposed the costs of dependence on a single maritime chokepoint, Manila’s strategic calculus around supply chain diversification and allied logistics integration has been validated. Japan’s role as the LEC’s primary financier mirrors the EU’s in IMEC: institutional credibility and financial depth that the US-Philippines bilateral relationship alone cannot provide, and a strategic self-interest in containing Chinese Indo-Pacific logistics dominance that is indistinguishable from Tokyo’s own supply chain security imperatives. The LEC’s principal vulnerability remains domestic: Manila’s alignment with Washington oscillates with electoral cycles, and the elite coalition – Ayala Corporation, Filinvest Land – that has profited from the geopolitical pivot could be disrupted by the same dynamics that enabled it.

Zangezur – The Corridor the War Is Accelerating

Of the three theatres, the Zangezur Corridor is where the Iran-Israel-US war has produced the most direct strategic acceleration. The proposed transit link connecting mainland Azerbaijan to its Nakhchivan exclave through Armenian territory emerged from a US-facilitated Armenia-Azerbaijan peace declaration in 2025. Its strategic purpose is to drive a wedge into the Russia-Iran-China logistical triangle in Central Asia – displacing Moscow’s security arbitration role in the Caucasus and weakening the Iran-backed Aras Corridor that has served as a resilient alternative to Western-controlled transit routes.

Iran’s direct military exposure in its confrontation with Israel and the United States has made it a more urgent strategic target in the Caucasian theatre precisely because it has made the cost of Iranian logistics dominance visible. A corridor that bypasses Iran-affiliated routes and reduces Tehran’s transit leverage is now not merely a long-term geoeconomic preference but an immediate operational priority for Washington. Azerbaijan, the corridor’s pivotal actor, has moved with corresponding decisiveness. Baku supplies 40% of Israeli crude oil imports – exports that rose 28% in the first half of 2024 even under intense regional pressure – and holds multi-billion dollar defense contracts with Israel, including Barak MX surface-to-air missile systems that have materially upgraded Azerbaijani military capability. In March 2025, SOCAR acquired Israeli drilling licenses for Mediterranean gas extraction: the only such agreement concluded by a state energy company from a Muslim-majority country in the post-October 7 environment. By early 2025, Israel, the United States, and Azerbaijan were in active negotiations over a formal trilateral cooperation framework spanning security, energy, and diplomacy – the corridor’s strategic logic expressed in institutional form.

Armenia faces the sharpest dilemma. The corridor passes through its sovereign territory, and the economic returns from transcontinental integration are offset by sovereignty risks and the collapse of Russian security guarantees that Moscow’s failure to intervene in the 2020 and 2023 Karabakh operations laid bare. The US-facilitated peace process offers Armenia an alternative security patron – but at a political cost that remains deeply contested domestically. Georgia, meanwhile, risks losing its existing hub status as the primary overland conduit connecting Azerbaijan to Turkey if Zangezur cargo flows divert southward; Tbilisi’s latent resistance is a corridor management challenge that sustained US diplomacy must address. Turkey, characteristically, plays both sides: promoting BRI-aligned alternatives to IMEC on the Mediterranean arc while aligning with Azerbaijan on Zangezur, where its own transit hub aspirations are served by the corridor’s success.

War, Corridors, and the Connectivity Paradox

Taken together, the three corridors reveal both the strategic coherence and the structural fragility of Washington’s tripartite infrastructure alliance. The coherence is real: IMEC, the LEC, and Zangezur each target a distinct node of Chinese and Russian hub-node dominance, they collectively span the three most contested geoeconomic theatres of the current era, and the Iran-Israel-US war has – paradoxically – accelerated alignment in two of the three theatres while disrupting the third. Gulf states that were hedging now need to choose. Azerbaijan is deepening. Manila is clarifying. Only IMEC’s Northern arc – the corridor most directly exposed to the conflict’s physical geography – is stalled.

The fragility is equally structural. Quantitative analysis of trade flows across corridor-affected country pairs shows positive but statistically non-significant average treatment effects on bilateral merchandise trade: the corridors have repositioned the geostrategic architecture of Eurasian connectivity – port centrality scores have shifted, investment frameworks exist, institutional commitments are on paper – but have not yet generated the self-sustaining commercial flows that would make structural repositioning durable. The geostrategic argument has been won. The economic argument has not. And the war is sharpening rather than resolving that paradox: by making strategic alignment more urgent, it is simultaneously making commercial normalization – the prerequisite for trade-flow generation – harder to achieve in the corridor theatre most central to the entire project.

The Age of Unpeace is not an academic abstraction. It is the operating environment in which every state enrolled in Washington’s tripartite corridor alliance is currently functioning – from Mumbai to Manila, from Aqaba to Yerevan, from Athens to Baku. The Iran-Israel-US war has not invalidated the connectivity strategy. It has tested it, stress-fractured one of its three theatres, accelerated alignment in the other two, and exposed with unusual clarity both the strategic logic and the structural fragility of the entire enterprise.